Managing the Financial and Emotional Cost of Forgotten Bills and Impulsive Buys

-

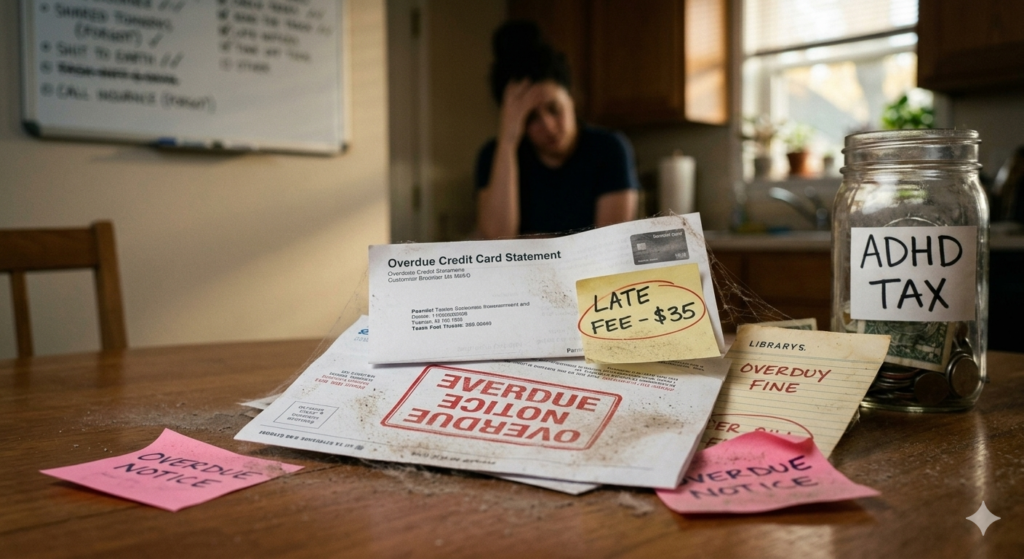

For many adults living with ADHD, the “ADHD Tax” is a recurring, unbudgeted expense. It isn’t a literal government levy, but rather the cumulative cost of executive function challenges: the late fees on a forgotten utility bill, the interest on a credit card balance, or the “hobby graveyard” of expensive equipment purchased during a fleeting moment of hyperfocus.

While the financial impact is quantifiable, the emotional toll—shame, anxiety, and a sense of inadequacy—is often much heavier. Understanding the mechanics of the ADHD Tax is the first step toward reclaiming both your budget and your peace of mind.

The Anatomy of the ADHD Tax

The ADHD Tax typically manifests in two primary ways:

- The Cost of Inattention: This includes late fees, lapsed subscriptions you forgot to cancel, and the price of replacing lost items. When the brain struggles to track deadlines or organize physical space, money essentially “leaks” out of your accounts.

- The Cost of Impulsivity: ADHD is often characterized by a search for immediate dopamine. This can lead to “doom spending” or impulsive purchases that provide a temporary high but result in long-term financial strain and clutter.

Strategies for Mitigation

Minimizing the ADHD Tax requires moving away from “trying harder” and toward building systems that work with your brain’s natural wiring.

- Automate Everything: If you can’t forget it, you can’t be penalized for it. Set every recurring bill to autopay and use calendar alerts for annual renewals.

- The “Wait-and-See” Buffer: Create a mandatory 24-hour waiting period for online purchases. Often, the impulse to buy fades once the initial dopamine spike subsides.

- Externalize Your Memory: Don’t rely on your “mental whiteboard.” Use apps, visual trackers, or even a simple whiteboard on the fridge to keep financial obligations in your line of sight.

Moving Past the Shame

The most expensive part of the ADHD Tax is the belief that these financial hurdles are a moral failing. They are not. They are symptoms of a neurobiological difference.

By treating these challenges as logistical problems rather than character flaws, you can approach your finances with the objectivity needed to make lasting changes. Resilience isn’t about never paying the tax again; it’s about narrowing the margin and forgiving yourself when a mistake inevitably happens.

-

For many adults living with ADHD, the “ADHD Tax” is a recurring, unbudgeted expense. It isn’t a literal government levy, but rather the cumulative cost of executive function challenges: the late fees on a forgotten utility bill, the interest on a credit card balance, or the “hobby graveyard” of expensive equipment purchased during a fleeting moment of hyperfocus.

While the financial impact is quantifiable, the emotional toll—shame, anxiety, and a sense of inadequacy—is often much heavier. Understanding the mechanics of the ADHD Tax is the first step toward reclaiming both your budget and your peace of mind.

The Anatomy of the ADHD Tax

The ADHD Tax typically manifests in two primary ways:

- The Cost of Inattention: This includes late fees, lapsed subscriptions you forgot to cancel, and the price of replacing lost items. When the brain struggles to track deadlines or organize physical space, money essentially “leaks” out of your accounts.

- The Cost of Impulsivity: ADHD is often characterized by a search for immediate dopamine. This can lead to “doom spending” or impulsive purchases that provide a temporary high but result in long-term financial strain and clutter.

Strategies for Mitigation

Minimizing the ADHD Tax requires moving away from “trying harder” and toward building systems that work with your brain’s natural wiring.

- Automate Everything: If you can’t forget it, you can’t be penalized for it. Set every recurring bill to autopay and use calendar alerts for annual renewals.

- The “Wait-and-See” Buffer: Create a mandatory 24-hour waiting period for online purchases. Often, the impulse to buy fades once the initial dopamine spike subsides.

- Externalize Your Memory: Don’t rely on your “mental whiteboard.” Use apps, visual trackers, or even a simple whiteboard on the fridge to keep financial obligations in your line of sight.

Moving Past the Shame

The most expensive part of the ADHD Tax is the belief that these financial hurdles are a moral failing. They are not. They are symptoms of a neurobiological difference.

By treating these challenges as logistical problems rather than character flaws, you can approach your finances with the objectivity needed to make lasting changes. Resilience isn’t about never paying the tax again; it’s about narrowing the margin and forgiving yourself when a mistake inevitably happens.